Every regional operator knows their serviceable address count. It goes into the board deck, sets the penetration targets, drives the investment thesis. The problem isn’t the number itself. It’s what operators assume the number means.

Footprint data tells you where your network runs. It doesn’t tell you who lives inside it, which households are about to lose patience with their current provider, or what combination of offer and channel is most likely to move them. Those are different questions. Most operators aren’t asking them.

Knowing a household exists is not the same as knowing what it will take to win it

A serviceable address count is a technical boundary. It defines the universe of homes your network can reach. “Reachable” and “convertible” are two different things, and conflating them is one of the more expensive habits in the industry.

The footprint number doesn’t tell you the household composition behind each address. It doesn’t tell you which homes are under contract with a competitor, which are on promotional rates about to expire, or which are genuinely dissatisfied with their current service. It doesn’t tell you whether a direct mail piece or a digital campaign is more likely to land.

An operator who passes 80,000 addresses and has captured 22% penetration has a data question as much as a sales question. The 62,400 homes they haven’t won aren’t a uniform group. Treating them as one is where spend goes to die.

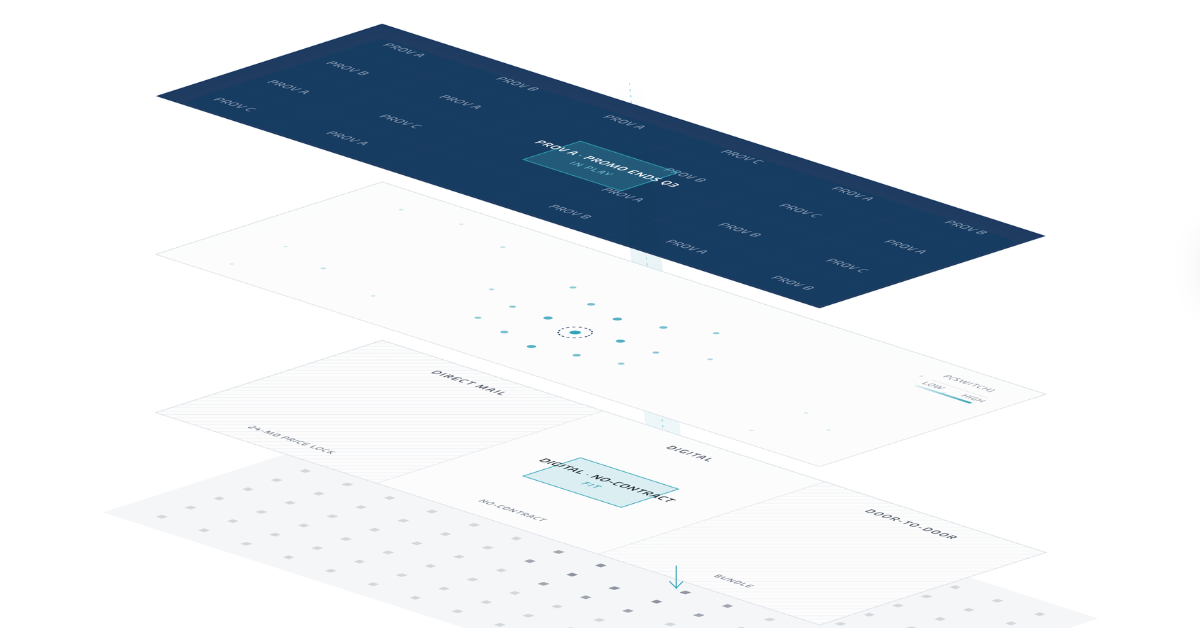

Three things high-growth operators know about every address in their footprint

Start with competitive exposure, because it’s the most actionable. Who is the current provider, and how stable is that relationship? A household whose promotional rate expires next quarter is a different prospect than one in year one of a new contract. These homes are genuinely in play. Most operators can’t identify them at the address level.

Propensity is the second layer, and often more useful than operators expect. Not every household in a footprint is reconsidering their provider at the same time. A household that signed up during a competitor’s aggressive promotional push 18 months ago may be quietly building a case to leave. One that just renewed is not. Propensity modeling identifies which homes are most likely to switch, and when. Without it, spend is distributed by geography rather than conversion probability.

Channel and offer alignment is where a lot of otherwise good campaigns go sideways. Some households respond to direct mail. Others convert through digital. Some want a no-contract plan; others want price certainty for 24 months. Without household-level intelligence, campaigns are uniform. The market isn’t.

When all three are missing, every address in the footprint looks equally worth chasing. The ones that aren’t will happily absorb your budget.

The channel isn’t broken. The targeting underneath it is.

When penetration targets are missed and response rates vary sharply between comparable markets, the instinct is to reach for the channel mix. Should we shift budget to digital? Is the direct mail creative underperforming? These questions assume the targeting underneath is sound.

It usually isn’t. The industry’s spend data makes that hard to argue with. Four of the top 10 global advertisers by spend are cable and telecom providers. Yet the industry carries some of the lowest marketing efficiency of any sector: high customer acquisition costs, low customer lifetime value, spend disproportionately concentrated in broad-reach formats. When you don’t know which households are actually in play, the rational move is to reach everyone. That’s what those numbers describe.

Swapping channels doesn’t change that equation. It just recycles the problem somewhere else.

High-growth operators don’t outspend the competition. They out inform it.

The regional operators with the strongest penetration growth aren’t outspending the competition.

They’re out informing it.

According to EY’s 2025 FTTH market analysis, the highest-performing providers build “detailed sales effectiveness tracking at granular geographic and competitive levels” and use that data to drive market-by-market decisions.

They know which homes in their footprint are most exposed to competitive disruption and concentrate spend there first. They build propensity models that surface the right households at the right moment. They match offer structures to what individual segments actually respond to.

The result isn’t a larger budget. It’s a better-aimed one. And the payback comes faster than most operators expect.

Learn how to build the intelligence foundation to hit your penetration targets

The serviceable address count is the starting point, not the finish line. Operators who treat it as the finish line are running a broad playbook in a market that rewards precision.

If you’re hitting targets in some markets and not others and can’t explain why, the answer is almost always in the data, not the channel. On May 27th at 1:30 PM ET, Pierre Elisseeff will walk through how high-growth operators have closed this gap and what it’s meant for subscriber growth and CAC.